Climate finance has become an increasingly discussed topic and is set to become one of the largest sources of funding in the coming decades. A broad range of entities will be offering climate finance from private companies to public institutions and financial organisations, it is only a matter of time. Given the challenges that lie ahead, Individuals and the private sector will benefit from it. However, this is still a niche topic: the #climatefinance hashtag only has 5,000 followers on a professional network like #LinkedIn. So, what is climate finance? What is its purpose? How does it work? Where is it coming from? Where does it go to?

Climate finance is generally presented as an expert topic with fancy concepts, but it is in fact very simple. Let’s begin with a simple definition. Climate finance is the use of financing instruments specifically aimed at reaching climate change mitigation and adaptation goals. In other words, climate finance consists in any financial efforts to support the reduction and avoidance of further greenhouse gas emissions getting into the atmosphere but also helping people and countries to prepare and adapt to different climate. This concept has been around mostly since 1997 with the adoption of the Kyoto Protocol.

Where is climate finance coming from?

While there is no historian to tell us when the term climate finance was first coined, it is generally accepted that the use of the term ‘climate finance’ began during the Earth Summit of 1992 which ended with the creation of the United Nations Framework Convention on Climate Change (UNFCCC) and later led to the drafting and adoption of the Kyoto Protocol in 1997. The word finance is only mentioned once in the UNFCCC and once in the Kyoto Protocol[1] and the then financial mechanisms that could be considered early forms of climate financing were not call so at the time. It is only with the Marrakesh Accords of 2001 that the word finance, mostly used in relation to adaptation, was finally mentioned[2].

Surprisingly, it is only as late as 2014 that the UNFCCC adopted an official definition for climate finance: “climate finance aims at reducing emissions, and enhancing sinks of greenhouse gases and aims at reducing vulnerability of, and maintaining and increasing the resilience of, human and ecological systems to negative climate change impacts”. In 2015, 4 mentions of climate finance fought their way through into the Paris Agreement[3].

Where does climate finance fit?

For the general public, climate finance can be considered as a fairly vague or broad concept. In order to further investigate what climate finance refers to, it is useful to first describe where it fits in the broader financing landscape. In order to do so I have sought to draw its family tree below. If it was a living thing, the climate Finance family’s genealogy could look like this.

As a caveat, this diagram does not represent all the extended family but the most notable members. It probably also does not fully capture the linkages between all its members. As you can see there is no space for green finance, since this can be perceived very generic, undefined, overused and tainted that it does not make too much sense to use it anywhere. All economic activities have an environmental impact, since there always is an ecological footprint behind the transformation of materials for the purpose of producing a good or a service.

Over the past 2 years, the European Union’s Technical Expert Group (TEG) on Sustainable Finance has gone through a complex and long process of defining what sustainable finance is, in order to facilitate the channelling of funding to it. The outcome was a sustainable finance taxonomy.

In short, financing climate mitigation in the EU context would correspond to fund activities that:

Are low carbon (even though this is usually poorly defined)

Contribute to a transition to a net-zero emissions economy but are not currently close to a net-zero carbon emissions level

Enable low-carbon performance by others or enable substantial emissions reductions through avoided emissions

The TEG has defined activities contributing to climate change adaptation as activities that:

Include or provide adaptation solutions that contribute substantially to preventing or reducing the risk of adverse impact or substantially reduce the adverse impact of the current and expected future climate on other people, nature or assets

The TEG even came up with a technical annex[4] listing all the activities contributing to mitigation or adaptation as well as a list of activities by sector.

Mitigation and adaption do not belong to a specific set of activities or sectors. It applies to all sectors and reaching the objectives of the Paris Agreement will require a substantial shift of our economy and of our lifestyles, and this partly explains the need for visionary politicians and leaders who are committed to implementing these objectives.

Why do we need climate finance?

In 2017, the OECD estimated that, globally, a shiny EUR 6.3 trillion a year would be required to meet the Paris Agreement goals by 2030[5]. To give an idea, this is slightly less than the monetary value of all of Germany’s global economic activities in 2019 and more than France’s or the UK’s for the same year.

It is obvious that the already overstretched public resources will not be sufficient to address this challenge. Whether you consider capitalism as an obstacle to achieve the Paris Agreement’s objectives or not, institutional and private capital will be necessary to get there.

Money has always been the sinews of war. The war the world finally seems ready to start fighting, is the one against a changing climate, in other words, against the unpredictable consequences of elevated concentrations of greenhouse gas in the atmosphere. It also a war that is meant to enable humanity to adapt to a new environment. An environment that may change to an extent that is still difficult to imagine.

Except maybe for conservationists, in our human-centred conception of the world, climate change has never been so much about the environment than about the human impacts these changes may trigger in that environment.

Even a 2°C hotter climate would trigger changes such as more intense extreme weather events (droughts, flooding, storms, heatwaves), a number of diseases migrating into temperate zones, global agricultural yields decreasing, lands becoming unfit to grow anything, water scarcity, generalized loss of biodiversity, ocean acidification and coral bleaching. All these having consequences on their own, on each other and combined, to an extent that would comparatively exceed those caused by the COVID-19 global pandemic.

The figure below shows that our current development pathway leads us to 3°C to 4°C of global average temperature increase. This could translate into +10°C in certain places and -10°C in others.

Until mainstream finance is not forced to integrate the safeguarding of our environment as a compulsory criterion in its decision to allocate funds, we cannot realistically hope to keep temperature increases below a reasonable level.

Whether it is to avoid dramatic climate change or to build resilience and cope with the effects of climate change, financing mechanisms will be increasingly in need. It is currently being distributed under very small and modest channels.

What does climate finance look like?

If you are still wondering what all this is about, wait no more. According to the Climate Policy Initiative, as summarised in the figure below climate funds are being expended through regular-rate (commercial) and lower-rate loans (concessional). Climate funds are also distributed as capital for companies to operate and project to enable them to start off and obtain further assistance if required. Finally climate finance also takes the form of grants to help fund technical and financial assistance for projects with no other access to financing.

One of the interesting resources in the area of climate solutions is the Drawdown Review[6]. While it only covers mitigation and some aspects of its methodology could be questioned, it is a very credible piece of work that contains a lot of insightful content.

According to the review, the following actions would have the greatest potential for reducing emissions:

Energy: cleaner electricity generation (e.g. wind power, solar, geothermal, biomass, waste-to-energy, etc.), energy efficiency (e.g. in lighting, building heating, insulation)

Agriculture: reducing food waste, meat and dairy consumption by developing plant-based food, protecting and restoring ecosystems (e.g. rewetting peatland, protecting primary forests and grassland, securing indigenous people land tenure rights, etc.), reducing the use of nitrogen fertilizers and improving rice production techniques

Industry: phasing out some refrigerant gases (e.g. in storing), recovering gas from waste (liquid and solid), recycling, and producing lower-carbon cement and bioplastics

Transportation: developing alternative to individual cars (e.g. public transit, carpooling, bicycle infrastructure, etc.), developing electric vehicles, energy efficient trucks and aviation

Building: adopting energy efficient cooking stoves, heat pumps, biogas for cooking, solar water heater and insulating buildings

The other part of the mitigation equation is the sequestration of carbon in natural ecosystems: through forestry, improved agriculture practice and restoration of ecosystems.

Two other channels used to disseminate climate finance are:

The carbon offset markets: where projects are provided payments for each tonne of CO2 equivalent they reduced or avoid. These payments could not really fall into the regular type of financial instruments and represented nearly 300 million USD in 2018 according to the State of the Voluntary Carbon Markets 2019.

The international climate funds: such as the Green Climate Funds, the most significant financing mechanism of the Paris Agreement, which has committed more than 6 billion USD since its inception a few years ago. The funding was provided mostly in loans and grants.

Since it is now clear mitigation efforts have not been enough, financing climate change adaptation has become an increasingly pressing issue. However, not only has climate change adaptation financing received less attention, it is also a lot more complex to quantify and monitor. Financing efforts in the field of adaptation has mostly taken the form of water and wastewater management, climate-smart agriculture (e.g. productivity increase, drought resilient crop, mixed crop-livestock systems, etc.) and disaster risk reduction. These efforts have been mostly funded by government and international or regional development agencies (e.g. development banks, UN agencies, climate funds, etc.).

How big is climate finance?

The think tank Climate Policy Initiative has been mapping climate finance flows since 2013 and found that in 2017-2018, around 579 billion USD were spent annually on average[7]. The yearly variation is presented in the figure below. Fund sources accounted in this data are very likely not exhaustive but include a very broad range of references.

As you may have guessed, when compared to the OECD estimation of what would be required to attain the Paris Agreement climate objectives, we are more than 90% short on funding. We would need another 5,7 trillion USD each year on top of what we are currently spending. The world is incurring delays every year on the level of investment required to put us on track to achieve these objectives.

Who spends climate finance? Who benefits from it?

According to the same Climate Policy Initiative report and as can be seen in the graph below, climate finance is coming from a broad range of sources.

Since we know countries themselves don’t have pockets that are deep enough to bear the burden of the heavy investment required, public finance should ideally only be used to leverage private finance if we want to reach the target amounts. However, private finance only accounted for 56% of all sources of climate finance in 2017-2018, which is far behind where it needs to be.

Climate Policy Initiative reported that domestic, bilateral, and multilateral development finance institutions (DFIs) accounted for most of public finance. DFIs, operate mostly in developing countries and are also providing development finance which is sometimes redirected or rebranded as climate finance. It also means that industrialized countries who also need public support benefit less from it and in a different form.

The remaining funds coming from public organisations is provided by regional and municipal governments and helps subsidise or invest into lower-carbon infrastructure.

Private finance has a more diversified range of sources. Private companies account for the majority of private investors, and commercial financial institutions play an increasingly important role. Aside from these, private individuals are also contributing to climate financing. They provide10% of the total amount spent. Lagging behind these actors are actually the most important financial actors: those with vast amounts of money, who manage households’ savings and retirement pensions. These actors do not seem to believe that the risks involved in building tomorrow’s world are worth taking. Thus, institutional investors and smaller funds managers account for a surprisingly small fraction (2%) of climate finance.

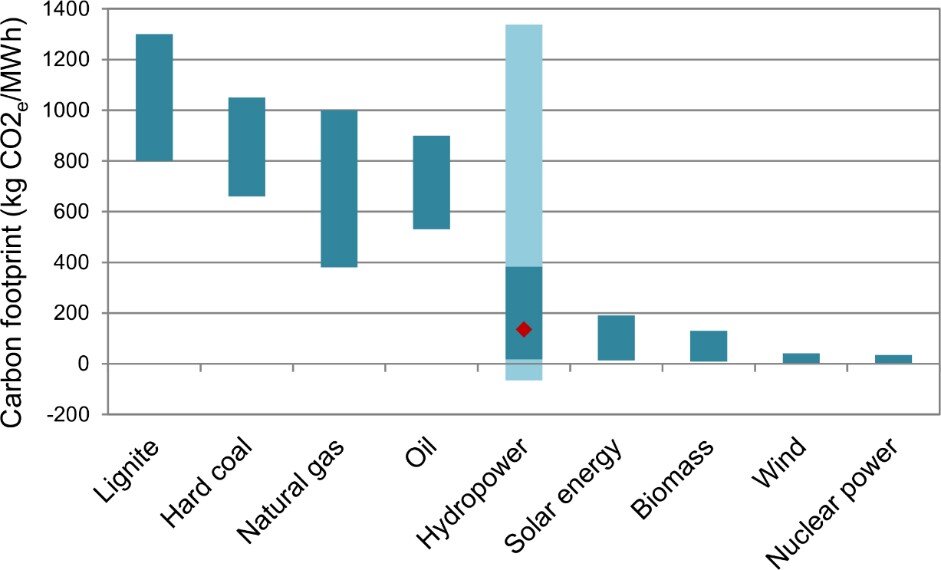

When it comes to the sectors towards which private finance is being channelled, renewable energy comes first (85%) notably for electricity production, followed by low-carbon transportation systems (14%). However, collecting data for some of these sectors can be difficult. This is highlighted in the graph below which also shows, an illustration of the narrative bias related to the role of renewable energy. It is indeed commonly believed that renewable energy will play a key role in combating climate change by enabling the clean generation of electricity even though it only accounts for 7.5% of energy consumed worldwide[8].

The figure below offers a rather tortuous view of where funding tagged as climate finance comes from and where it goes. It does however provide a complete picture of the current situation.

Conclusion

While still a fairly niche practice, climate finance is increasingly used by the public and the private sector. A growing number of projects can take advantage of the opportunities this shift will create. We believe it is now the right time for projects, programmes and organisations to identify potential sources of funding or activities that could enable them to implement mitigation and adaptation activities. It is also the right time for financial organisations to build up their climate finance offering to the general public.

The Drawdown project estimates that overall, net operational savings exceed net implementation costs four to five times over when most mitigation measures are implemented. This means that with the right financing instruments, our societies could unleash a broad range of opportunities to fight and adapt to climate change.

HAMERKOP’s experts have more than 12 years of experience helping companies, NGOs, and governments navigate the complexity of climate finance, from identifying candidate initiatives, assessing projects, liaising with the right source of funding and drafting winning project proposals. If you are looking to engage with climate finance, whether to benefit from it or provide funding, we can help, so reach out to us.

—-

[1] The Kyoto Protocol: https://unfccc.int/sites/default/files/resource/docs/cop3/l07a01.pdf

[2] The Marrakesh Accords: https://unfccc.int/cop7/documents/accords_draft.pdf

[3] The Paris Agreement: https://unfccc.int/files/essential_background/convention/application/pdf/english_paris_agreement.pdf

[4] Technical annex: https://ec.europa.eu/info/sites/info/files/business_economy_euro/banking_and_finance/documents/200309-sustainable-finance-teg-final-report-taxonomy-annexes_en.pdf

[5] OECD. 2017, Investing in Climate, Investing in Growth, OECD Publishing, Paris, http://dx.doi.org/10.1787/9789264273528-en

[6] The Drawdown Review 2020: https://www.drawdown.org/drawdown-framework/drawdown-review-2020

[7] The Global Landscape of Climate Finance 2019. https://climatepolicyinitiative.org/publication/global-landscape-of-climate-finance-2019/

[8] Long-term energy transitions, Portugal, 1856 to 2008. https://ourworldindata.org/grapher/long-term-energy-transitions