Looking for a climate friendly current bank account in the UK

A few months ago, I was looking to open a bank account in the United Kingdom. Being a part of the British Standards Institution’s sustainable and environmental finance group and having worked on various issues related to the decarbonisation and climate resilience of the financial sector, I am only too aware of the issues. I have consequently decided to only patronise the business of a bank or of a financial services provider with clear policies and activities not contributing further to climate disruption.

Banks, as well as pension and investment funds, are increasingly in the spotlight for their contribution to climate change. Money on your bank accounts or pension fund is potentially invested in arm manufacturing, mining, tobacco or other harmful industries.

The consumption of any good or services has an environmental footprint and the footprint of your money is not restricted to the materials and energy required to manufacture bank notes and coins. It is also and very much more what your money is used for. As illustrated by the recent findings of the UK Parliament’s environmental audit committee, it is not credible to claim you have decreased your emissions at home if you are sending billions of pounds of taxpayer money abroad to build fossil fuel burning power plants[1].

As of June 2019, 183 (out of 194) nations have ratified the Paris Agreement that aims to keep the increase in global average temperature to well below 2°C above pre-industrial levels and to limit the increase to 1.5°C. Governments have made ambitious pledges which require reductions of greenhouse gas emissions by at least 80% of 1990 levels by 2050.

However, while over the years pledges have piled up quicker than plastic waste in the ocean and the amount of public, private and civil society initiatives have increased almost as much as global concentration of greenhouse gas emissions into the atmosphere, we are still at least a degree off the less ambitious target.

The financial sector at the forefront of the battle

The financial sector has helped drive the carbon-intensive society we live in. It now has the chance to fuel the development of low-carbon technologies and climate-resilient activities.

While divesting existing fossil fuel assets is not enough in itself and may not always trigger the expected results (assets may simply change hands), some actors in the financial industry have already began their portfolio divestment, driven by potential reputational and financial risks. Divestment opportunities have been further enhanced as funding cleaner technology has become more aligned with investor requirements (i.e. higher returns, lower risks).

Too many are banking on the climate crisis

Recently, an alliance of NGOs, including Bank Track and the Rainforest Action Network, has published Banking on Climate Change[2]. This report found that 33 global banks have financed fossil fuels with $1.9 trillion since the Paris Agreement was adopted (2016–2018), with the biggest contributors outlined below:

Tar sands oil: RBC, TD, and JPMorgan Chase

Arctic oil and gas: JPMorgan Chase, Deutsche Bank and SMBC Group

Ultra-deepwater oil and gas: JPMorgan Chase, Citi, and Bank of America

Fracked oil and gas: Wells Fargo and JPMorgan Chase

Coal mining: China Construction Bank and Bank of China

Coal power: Bank of China, ICBC, Citi and MUFG

The figure below provides a visual view of this tainted ranking.

As you can see, the big European banks are not far behind the American, Chinese and Japanese ones. Paradoxically, a few of these companies have policies restricting financing for coal mining. There are 4 British banks (Barclays, HSBC, Royal Bank of Scotland and Standard Chartered) in the top 33 banks financing over 1,800 companies active across the fossil fuel life cycle.

Although things are changing, with banks like Royal Bank of Scotland and HSBC working on their policy to restrict financing to some of these assets, such a move remains too slow and poorly aligned with the required efforts.

In 2016, ChristianAid published a report[3] assessing the UK’s largest banks and their alignment with the Paris Agreement. They then graded their performance on policies to accelerate the shift to a low-carbon economy. As you can see in the table below, the large banks perform poorly, with a lack of transition plan, investments in fossil fuel and a lack of carbon footprinting for some or most of their lending, as the main drivers.

The banks on the climate blacklist

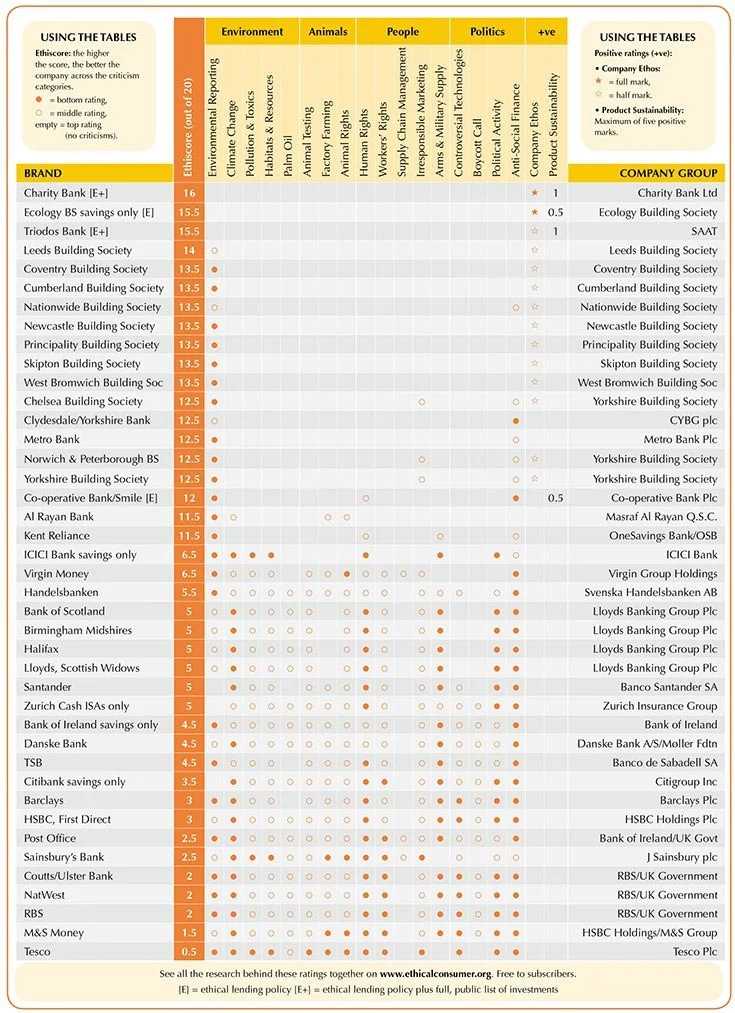

According to the Ethical Consumer[4], an independent and not-for-profit co-operative, 80% of people’s bank accounts are with the big five banks, the same that have the lowest ranking on their ethical scorecards.

If you feel responsible for your money, it may seem logical not to bank with Barclays, HSBC, Royal Bank of Scotland, Standard Chartered and their affiliates: First Direct, M&S bank, Halifax, Bank of Scotland, NatWest and Ulster Bank.

You don’t need to be an activist to prevent the money in your bank account to be used for fuelling the climate crisis as you still have quite a few alternatives.

Ethical and climate friendly banks. Excuse me?

Choose Ltd, a credit broker, defines ethical banks as always aiming to have a positive social and environmental impact when seeking profits. In addition to these criteria, Ethical Consumer considers bank ethicality through animal rights, political and human rights credentials.

According to the criteria considered, top ethical banks varies:

Choose Ltd, without disclosing a methodology or rankings, mentions the following as ethical banks operating within the UK: Charity Bank, Triodos Bank, the Co-operative Bank, Handelsbanken, TSB and the Ecology Building Society as well as credit unions and the building societies (BS) in general;

The Good Shopping Guide[5], that compares ethical brands uses a 9 criteria matrix to find Ecology BS, Leeds BS, Newcastle BS, Allied Irish Banks, Coventry BS, Nationwide BS and Skipton BS to be ethical banks;

Ethical Consumer provides the most comprehensive assessment and considers tax avoidance, fossil fuel investments, investments in Israel as particularly harmful. Charity Bank, Ecology BS, Triodos, Leeds, Coventry, Cumberland, Nationwide BS and other BS, Clydesdale, Co-op, Metro Bank are the best rated and considered climate friendly. However, the only one that currently seems to invest seriously in renewables, is Triodos.

While Ethical Consumer is digging slowly into the climate impacts of banks, no specific research is publicly available on climate-friendly banks specifically.

Defining climate friendly financial service providers implies multiple and sometimes complex considerations:

Its climate change mitigation impact: does it invest into carbon intensive fuels or commodities driving deforestation (e.g. palm oil)? Does it contribute to financing a transition to a low-carbon economy? Does it measure the footprint of its lending activities? Or does it have a transition plan to phase out any carbon intensive investment?

Its climate change adaptation impact: does it help individuals or companies adapt to climate change and become more resilient? Does it ensure that when funding new infrastructure or project, they take into consideration climate models?

Its own direct impact: does it measure, report, reduce or even offset the impacts of its own operations? Does it have any specific policies to reduce its energy consumption and the impacts of its data centres?

And even though ShareAction, a charity promoting responsible investment practices, seems to be praising improvements in climate-related disclosure, information is still very patchy and not accessible to the mass. Transparency is key to fight the climate crisis.

The more climate virtuous banks and financial services

If you are in UK and looking for a bank account, you still have a few options for sustainable and ethical personal or business banking.

Building societies and credit unions

These are financial institutions owned by its members as a mutual organisation. They are often acting more ethically as regulations limit the amount of money they can invest in certain industries and because they invest their profits for the benefit of borrowers and savers rather than shareholders. In UK there are plenty of them, local for many, and the largest ones are: Nationwide, Cumberland, Yorkshire and Coventry Building Societies.

Credit unions are also considered ethical as they are financial co-operatives owned and run by their members.

Traditional banks

Banks not blacklisted for their climate-damaging activities include, but are not restricted to:

Handelsbanken, listed as an ethical bank by some but with investments in fossil fuel on possibly around 70% of their funds[6];

Danske Bank, a Danish bank active within the UK for which no assessment was carried out, but that has experienced a range of ethical discredits;

Bank of Ireland, while it has experienced a range of controversies and has an environmental policy, seems ambitious on paper in reducing the environmental impacts of its activities. However, it has not made any commitment to stop funding climate damaging activities;

Metro Bank, this new bank does not have a “bespoke environmental policy”, does not seem to have a clear and transparent investment policy and has not made any commitment to not fund climate damaging activities;

Yorkshire and Clydesdale Banks, although usually well ranked among ethical finance reviewers, these banks do not have specific restriction on banking with sector potentially damaging climate;

TSB, the bank that relaunched in 2013, uses money invested by their customers to fund loans and mortgages to local people and businesses and don't have an investment banking or corporate finance arm; and

Cooperative Bank, still the only major bank committed to fighting climate change and which states that it “will not provide banking services to any business whose core activity contributes to global climate change, via the extraction or production of fossil fuels (oil, coal, gas and shale gas), with an extension to the distribution of those fuels that have a higher global warming impact (e.g. tar sands and certain biofuels)”.

Modern financial solutions

In the digital era we live in, you now have even more options for banking. It actually no longer has to be a bank. There are mobile applications that offer, to some extent, similar services to traditional banks for an often more competitive package. These include CashPlus, Revolut, Coconut, Starling Bank, Anna Bank, Tide, Counting Up and Fair Everywhere. These banking services usually use customer deposits to lend to other customers as overdrafts and loans.

While these banks and financial services providers are not as bad as the big ones, you cannot guarantee they do not finance local business with climate unfriendly practices or make little effort to help finance climate change adaptation. In addition, the cumulated impact of their practices cannot be comparable to the damages caused by large banks.

Much is still needed for business and corporations to take stronger steps towards the global climate protection cause and provide the transparency their customers need to make informed choices.

Since choosing a bank or a financial service provider implies the consideration of multiple parameters, I cannot advise on a single option. However, as a rule of thumb, you could consider:

A building society or a credit union if you have one locally where you live and do not have fancy banking needs: Nationwide, Cumberland, Yorkshire and Coventry Building Societies seems to be all good options;

A bank that have made a clear commitment to fight climate change and offer a wider geographical coverage: Triodos seems to offer great integrity but Co-operative Bank would also work; and

An app-based service provider that will offer flexibility when travelling, making online purchases or having to connect with other web-based apps: Starling Bank and Monzo are both credible options.

When you can align your consumption choices with your values and take decisions that reinforce sustainable means of production and consumption while getting a better service, it is time to switch!

SOURCES:

[1] House of Commons Environmental Audit Committee, UK Export Finance, Nineteenth Report of Session 2017–19

[2] Banking on Climate, fossil fuel finance report card 2019 (Rainforest Action Network, BankTrack, Indigenous Environmental Network, Sierra Club, Oil Change International and Honor the Earth, 2019)

[3] Our future in their plans (ChristianAid, 2016)

[4] Ethical Consumer, current accounts: https://www.ethicalconsumer.org/money-finance/shopping-guide/current-accounts

[5] The Good Shopping Guide: https://thegoodshoppingguide.com/ethical-rankings-banking

[6] Handelsbanken sustainability report: https://www.banktrack.org/download/sustainability_report_2017_5/sustainability_report_2017_1.pdf